The squeeze on Australian finance firms

If you broker mortgages, advise on finance, or run a small fintech, you feel two forces at once. Clients want faster answers and a smoother experience. The rules want every step documented and defensible. You sit in the middle, with a lean team and no in-house AI specialists, trying to serve more people without dropping a single obligation.

The admin is the part that quietly eats the week. A broker rebuilds the same application details across a CRM, a lender portal and a spreadsheet. An adviser spends hours assembling a Statement of Advice when the thinking took a fraction of that. A small fintech wants to use its own data well and ship features, but the team is busy keeping the lights on. None of this is the work that wins or keeps clients, yet it fills the day.

The cost of a mistake is what makes it heavy. This is a Your-Money-Your-Life field. A wrong number in an application, a gap in a record, or data handled the wrong way is not a small slip. It can harm a client and put your Australian Financial Services or credit licence at risk. So the work has to be both faster and safer, and most tools promise only the first.

Why a tool on its own falls short

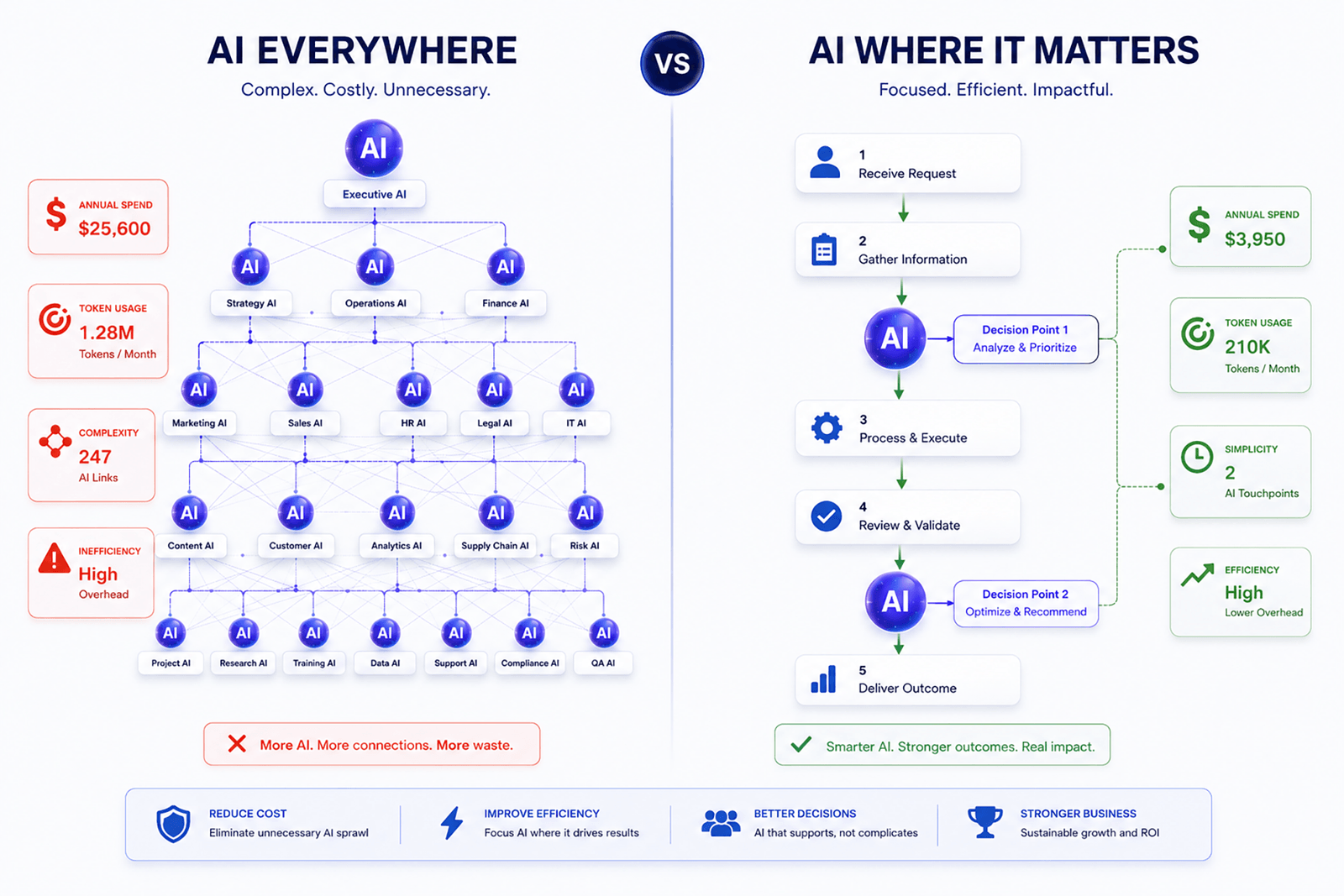

The usual instinct is to buy software, switch it on, and hope it sticks. In finance that approach tends to disappoint. A generic tool does not know your products, your clients or the obligations you carry, and a clever model that cannot show its reasoning is a liability the moment your licensee asks how an outcome was reached.

The harder issue is your data. When client and product information is scattered and inconsistent, any tool built on top of it inherits the mess. It produces output that looks confident and is quietly wrong, which is the worst result in a field where a wrong answer affects someone’s money. A tool is a starting point. The outcome comes from the foundations underneath it and a documented, repeatable process around it.

How we build it to last

We start with one painful process and build it to the standard your licensee expects. Three principles from our approach shape every step, applied to the specifics of your firm.

Training, security and governance come first. You hold client financial data and you carry licence obligations, so this leads everything we do. We set who can see what, how data is stored, and what the tool is and is not allowed to do, before we build a single feature. For a broker that means client details stay locked down and access is controlled. For a fintech it means the same discipline is engineered into your product from the start, in line with the Privacy Act.

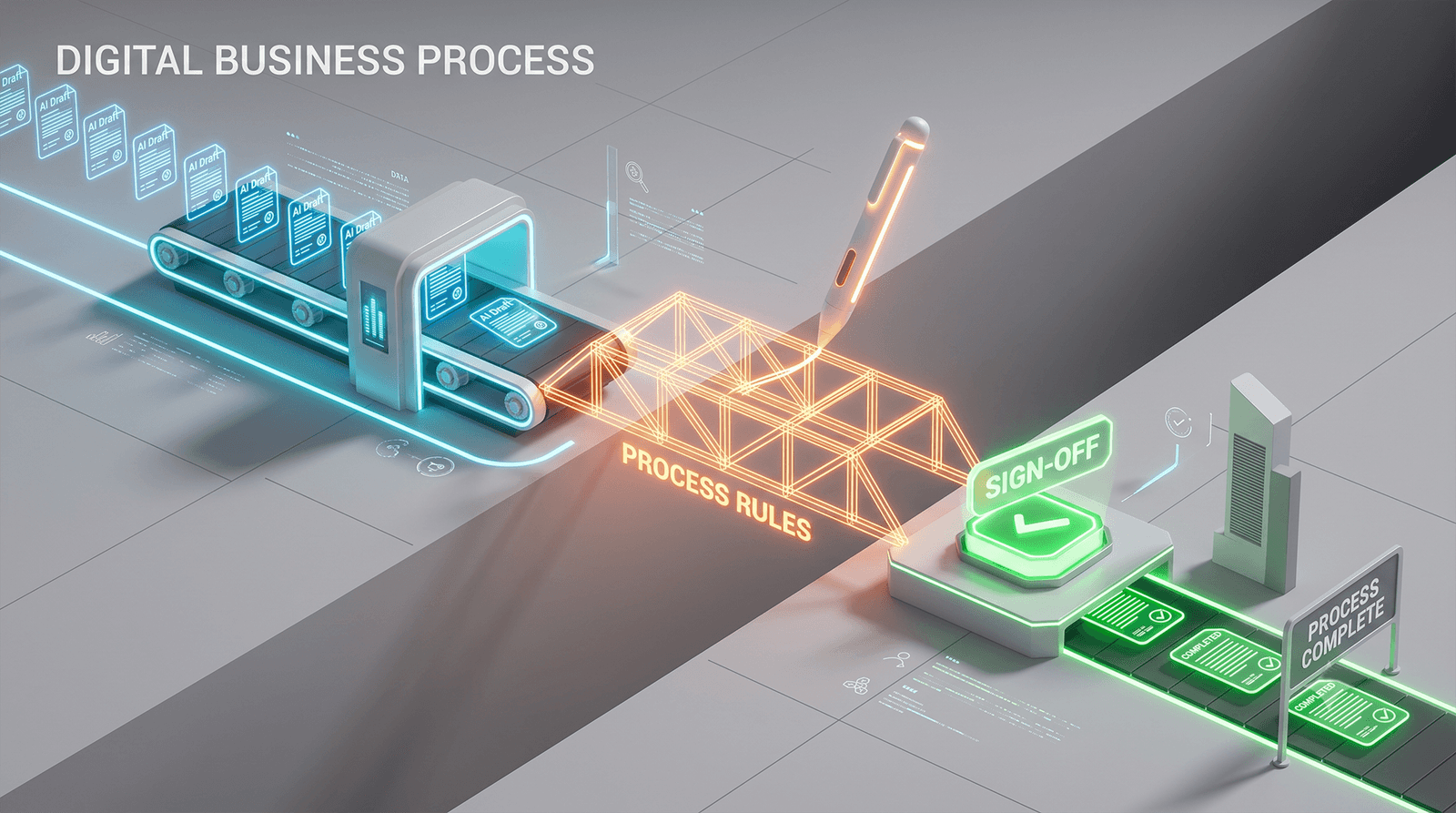

Decisions are version-controlled and documented. How a recommendation or a decision was reached is recorded and dated, the same way good engineering teams manage code. If a step changes, the change is logged and reversible. The result is a clear, time-stamped trail showing how each outcome came about, which is exactly what ASIC and your licensee will want to see, and what the Design and Distribution Obligations expect you to be able to demonstrate about who a product suits.

Your data ecosystem gets healthy. Before any AI is useful, your client and product data has to be clean and in one usable shape. We pull it out of the silos, fix the inconsistencies, and connect the systems that should have been talking all along, including the legacy core banking systems a fintech often has to work around. Once the data is sound, faster preparation and sharper analysis follow.

Every tool ships with logging, limits and human review built in. It is tested against your real past cases before it carries any load, so you see where it is right and where it is not before it touches a client.

Where the regulation sits

This is regulated work, so defensibility is a design requirement, not an afterthought. Advice and credit decisions stay with licensed humans. The AI does preparation, it does not advise and it does not decide. Nothing produced here is financial advice in itself, and a person who holds the responsibility signs off before anything reaches a client.

For brokers and advisers, the obligations under the National Consumer Credit Protection Act, including responsible lending, stay firmly with your accountable staff. The Design and Distribution Obligations sit across product work, so records show a product reached the right kind of client. Across both, personal and financial information is handled in line with the Privacy Act 1988, and the audit trail is built so your Australian Financial Services or credit licence obligations can be evidenced on demand. Because this is a Your-Money-Your-Life topic, a named human reviewer signs off on accuracy and compliance before anything is published or put in front of a client.

What changes for your firm

The aim is simple. Less time on paperwork, more time with clients, and product work that ships sooner, all without adding compliance risk. Application and advice preparation that took hours gets the routine parts handled in minutes, with a licensed person reviewing and approving. Client data lives in one clean place instead of five, so nobody re-keys the same details twice. Fraud and risk signals get sharper, even for a small team. Customer segmentation analytics point your effort at the clients and products where it pays off.

And under all of it sits the record. Every decision step is logged and versioned, so when a regulator or your licensee asks how an outcome was reached, the answer is already there. The same discipline that keeps you compliant also makes the work faster, because clean data and a clear process remove the friction that slowed you down.

We are deliberately careful in this sector. A tool you cannot explain is a risk to your clients and your licence, so we build for explanation and oversight first, and for speed within those bounds.

How AI applies across our work

The same foundations carry across sectors. See how we apply AI for employee productivity in AI Agents, and how clean data underpins everything we build in our approach.